Bitcoin is an environmental disaster - Part 1

Bring on the hate, coiners

Hello once again, friends. Today, we’re going to be discussing everyone’s favorite topic since 2017: Bitcoins!

I am working on some longform stuff about Bitcoin and crypto that touches markets, the fed, inflation, energy use and debt. But in the meantime, I want to make sure that there is no uncertainty where the ESG Hound stands on Bitcoin. It’s bad, folks. Let’s get started.

A few weeks ago, Wall Street darling and purveyor of interestingly constructed ETFs Cathie Wood, of Ark Invest, went on CNBC and stated outright that Bitcoin was “attractive” from an ESG standpoint.

Some of Ms Woods’ related thoughts on the matter were revealed in a Bitcoin Magazine interview in June. I’ll be citing some quotes to drive home the point.

Now, despite the title of this Substack, the ESG Hound is primarily an E (Environmental) guy. My interest in S & G (Social and Governance) is more how they overlap with Environmental concerns but should always be considered when discussing ethical investing.

The power usage of Bitcoin and Crypto has been discussed to death, perhaps to the point that the beaten horse has been reduced to a slurry of the basic carbon and salt elements. The ESG Hound discussed the carbon footprint of Microstrategy in this previous post. But more broadly, I want to discuss some fundamentals of LCA (life cycle analysis) and other techniques to demonstrate how ridiculous crypto arguments are.

Part 1 is today, parts 2 & 3 to come soonish.

1. Part 1: Energy is fungible and finite

I keep seeing the same form of argument from coiners regarding the massive power use (and related CO2e impact) from crypto mining. “WE’LL JUST GO GREEN!”

Cathie herself makes a form of the argument here:

"Putting bitcoin mining into a solar powerwall merchant power ecosystem so that it could absorb all the extra energy coming from the sun after the powerpack is filled up. That would add a new dimension of economics to this ecosystem and would encourage homeowners and utilities to add more solar than otherwise would be the case. So it's actually going to accelerate the movement into renewables. I think that's what's going to bring institutions back." - Bitcoin Mag Interview

Read this a few times. She’s still pushing consumption. I would, of course, expect no less from a fund manager who hawks equities trading at 30x revenues. Instead of burning coal, we’ll just use clean wonderful solar!

Now, of course, there is an embedded environmental cost with making solar panels. It’s one tactic that oil people love to repeat endlessly. I think we all understand that rare earth metals, sand, and heat (from usually natural gas) are combined to make solar panels. These activities have an embedded energy input as well as an embedded carbon footprint. This is simply fact. But if, over the life of the panel, it can produce more energy than it costs to make and can offset the input carbon, it should be considered A-OK for ESG purposes. Now, there are more intangible factors at play: the rarity of supplies as well as other impacts from production such as water pollution and mining impacts and air pollution impact the end “Good” derived from solar panels. This needs to be considered, but for now, we’ll accept that solar panels are generally ESG friendly.

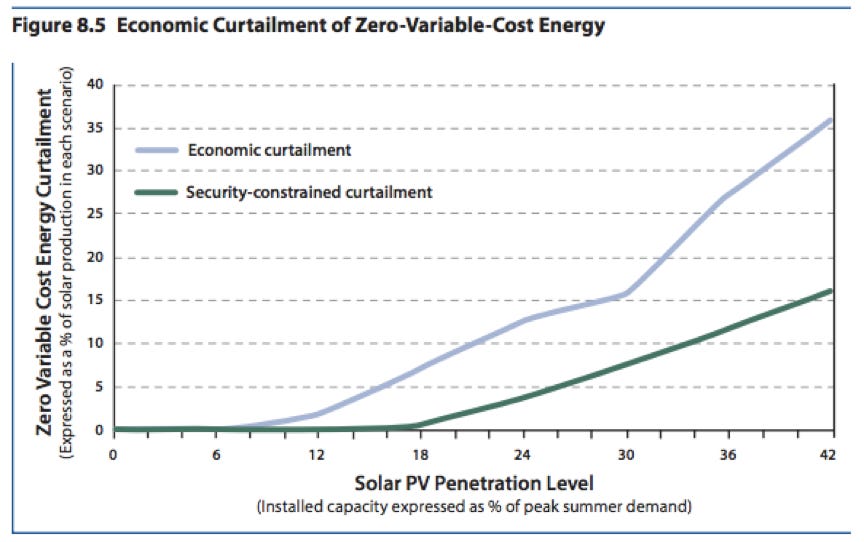

This is one of my favorite charts and I’ll explain why below

It shows both:

The incredible utility of solar

The inherent limitations of intermittent power sources (such as solar and wind)

Let’s start out by admitting a big issue here: Germany is not a great place to put solar installations. The PV fabs are resource limited and perhaps a country that is cloudy and at a suboptimal latitude shouldn’t have been soaking up so much of the supply when sunny places close to the equator would result in better global CO2 reduction. This touches at a fundamental problem with global environmental problems (Climate change, ocean trash/pollution, etc) vs local ones (Ozone levels, groundwater pollution, etc etc). Local environmental problems can and should be handled by local governments. Global problems need top down coordination and cooperation. We’re not good at doing this, as a species, yet.

Germany also famously shut down nuclear power facilities (the mother of all low carbon energy) and retrofitted coal plants to burn trees (yes, they really did!) in part to accommodate the surge in solar and wind installations. It goes without saying that The ESG Hound is not a huge fan of this philosophy, but that’s a tale for another post.

The point here is that the demand curve during the summer (when A/Cs are cranking and everyone is hard at work building stuff and writing code and having meetings), as reflected by price, nearly perfectly mirrored the electrical output curve of solar arrays. As a result, solar installations caused this time sensitive cost curve to flatten. Dramatically. This is cool, and good.

But what happens when you install too much solar? Well, Germany’s desire to go hog wild on PV led to some incredible price distortions on very sunny days. Wholesale power went and continues to go negative periodically, baseload energy sources (coal plants, nuclear) were basically not needed and the whole European grid was a nightmare. Natural gas engines, and to an extent turbines, can be ramped up and down as needed to meet peak demand. Nuclear is not this way. You can’t just dial down a nuclear reactor for a few hours because you don’t need the megawatts right now.

On the flip side, at night time, without sufficient baseload power, the incremental cost of a MWh essentially has no upper bound, as we Texans discovered earlier this year during a deep freeze event. Any inelastic demand coupled with zero supply will lead to essentially infinite costs. Thus the time value of energy needs to be considered. I will post more on this topic in the future, but for now I think it makes sense to most people, conceptually.

There was a very excellent series of posts from The Breakthrough Institute, one of my favorite sources for actual, realistic analysis of climate and technology in 2015 (linked here and here). I’ll let you read the posts yourself if you want, but the take home point was this:

The capacity factor threshold implies that wind may eventually be able to provide on the order of 25-35 percent of a power systems’ electricity, while solar may top out at 10-20 percent in most regions

Essentially, you’d have to install something insane like 300-400% of total peak rated capacity PV/Wind installs to meet the needs of the grid 24/7/365. A sober, realistically optimistic upper bound for intermittent sources of power such as solar and wind is therefore in the 40% (+/- 10) range

“WHAT ABOUT BATTERIES?” This is a topic I can (and will?) write thousands of words about. Utility batteries may have a place in the grid. They also might be largely greenwashing. But batteries as backup, from an energy standpoint are not a source of energy. They reduce the energy, financial and environmental returns of solar. For grid balancing and short term peak mitigation purposes, this might be ok, but as a grid wide alternative to the “solar night time problem,” they’re bad on any sort of large scale. So better batteries might push that 40% Wind/Solar value up to 45-50% (maybe), but that’s a big ‘ole TBD

Now, on to bitcoin.

Elon’s galaxy brain take here is bad and ties in nicely to Ms Wood’s insane declaration that Bitcoin is an ESG asset. The fact of the matter is, if:

Solar and Wind has an upper limit for economic and thermodynamic returns, and

There is no accompanying hydroelectric and/or nuclear deployment

Any bitcoin or crypto rig plugged into the grid, or that uses the finite supply of PVs available, takes away power from something actually useful for society, be it charging EVs, powering offices, running A/Cs, or performing life critical tasks such as, I dunno, powering a hospital ICU. Therefore, any incremental crypto mining created by market forces in crypto speculation will, by necessity, require additional fossil fuel demand and will, as such, contribute to increased Carbon emissions.

tl;dr There is no “green crypto” because, as stated in the prompt: Energy is both fungible and finite.

ESG HOUND OUT

Here are the upcoming posts, to be completed in the next week or two:

ESG Hound, I'm enjoying your substack a lot, albeit with some delay. Looking forward to part 2 and 3 of this series.

Now allow me to play devil's advocate:

- Germany does not use / need that much of AC: it never gets that hot there, so that solar energy will rather be needed elsewhere

- I would be curious to see a more recent graph of these prices ...

- In the long run, is an 'energy source' really "renewable" if it needs /rare earth materials/ ? I mean, by the time we've mined the economical part of it, we won't be able to use that 'energy source', are we ? how renewable was it then?

- "Battery" could simply be alpine dams (and pumping up), but this is not without environmental consequences...

- if Bitcoin or crypto is about an 'international payment network', then that could be the 'value' of it, as opposed to current speculation / ponzi stuff ... But I have yet to see the compelling numbers for crypto as 'international payment network'

- at the end of the day, I fully agree with you that crypto's energy and computation power gluttony could definitely be used better, even ESG-wise - medical research ? environmental research ? you name it ...