ESG Bites 12/8 - The Most Effective Regulator You’ve Never Heard Of

Mining For Risk

Every single time I scroll through a 10-K, the annual financial statement form for public companies, I always pause at a section that rarely has anything in it. And I smile.

I look through a LOT of 10-K’s. I work closely with people who do the same. Last week, I asked a few old-timers in the industry about “Item 4,” and the response was a resounding shrug. “It’s just a thing I never look at,” one told me. I spoke with a retired sell-side materials and mining analyst about Item 4; he had a different take. “There are often material dollar amounts listed in Item 4. Real liabilities. It’s a must-read,” he told me.

Ok, this makes sense on the surface. Most publicly traded companies in the United States do not operate Mines. But that doesn’t answer the question of *why* this item must be on every 10-K. There’s no required transportation safety section on a 10-k, nor an OSHA “general industry” or “construction safety” disclosure section. Likewise, a section on EPA or environmental disclosures is missing. Companies sometimes do disclose enforcement cases from DOT, EPA, OSHA, and other regulators. But that disclosure is voluntary and at management’s discretion if it meets the SEC’s nebulous definition of “materiality.”

Mining Safety Disclosures (Item 4) were added as a discreet, mandatory 10-K requirement for the SEC’s 2012 Dodd-Frank Act implementation.

(As an aside, Dodd-Frank also incorporated requirements from the 2009 Congo Conflict Minerals Act. This law was pushed by years of tireless NGO advocacy, but the 2006 movie “Blood Diamond” probably played a shockingly large role in passing legal disclosure requirements around mineral sourcing.)

During the Dodd-Frank lawmaking process, lots of focus was on mining companies, and when specific financial risks were discussed, one topic came up repeatedly:

MSHA.

Everyone’s heard of OSHA, but (in case the name wasn’t clear) the Mine Safety and Health Administration (MSHA) is the regulator for Mining Operations and mining operations only. The Occupational Safety and Health Act of 1970 helped make tremendous strides in US worker safety, but it wasn’t deemed sufficient for Mining operations, a notoriously dangerous industry. Congress decided in 1977 to pass the MSHA Act, which would create a parallel rule set and regulator.

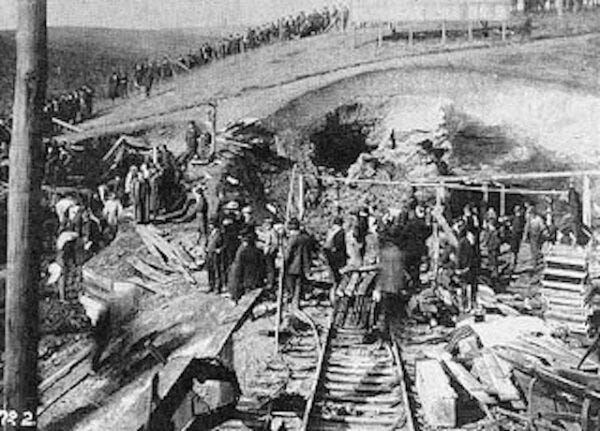

In 1907, two of the Monongah coal mines (units 2 and 8) in West Virginia exploded in a massive fireball after a railcar rolled backward into the mine entrance. The collision stirred up large quantities of coal dust, which found a spark and lit the mining complex up. 362 miners died.

Throughout the 1960s and 70s, as Americans began demanding more regulation on all manner of industries, a coal mine would explode every couple of months. Several times per year, the entrance to an underground mine would collapse, leaving a handful of American workers to suffocate or starve to death.

Passing the Mine Safety Act and forming MSHA was a no-brainer, and the results of regulation and better technology have yielded excellent results:

While OSHA had many generic requirements on rules and rulemaking and a framework for inspecting and regulating worker safety, The Federal Mine Safety and Health Act was an entirely separate beast. The law mandated inspection frequencies. OSHA only shows up when a serious complaint has been lodged (sometimes) or after someone has died (usually, but not always). Every licensed mine under the purview of MSHA gets inspected four times yearly. Fines and penalties are severe and swift. “MSHA inspectors don’t fuck around” is a common refrain.

While other federal agencies have prolonged investigations, negotiated orders, and several levels of bureaucratic review, MSHA is obligated to stop bad behavior before it becomes a problem. OSHA has languished in comparison, with the per capita number of Federal Safety inspectors shrinking every year since 1995. The Mine Safety Act doesn’t allow this. Four inspections per year, per mine, isn’t a goal. It’s law.

MSHA was further bolstered by the 2007 MINER Act, which was signed into law following the 2006 collapse of the Sago Mine, also in West Virginia. 13 miners were trapped behind a collapsed coal mine shaft for several days. Only one man survived. And in 2013, MSHA passed a new enforcement mechanism called its “Pattern of Violation Authority.”

Pattern of violations (POV) authority is arguably the most stringent enforcement tool Congress granted MSHA in the Mine Act. When the agency determines that a mine has a pattern of violations, MSHA is empowered to issue a withdrawal order for any subsequent S&S violation. MSHA will continue to issue such orders until the mine can get through a full MSHA inspection without any S&S violations. Being on POV status makes it extremely difficult for an operator to continue the operation of a mine.

When comparing fatal incident rates for Mining versus All Industries and Construction (one of the other very dangerous industries), the results speak for themselves:

So, getting back to the initial question. Why is Mining Safety the only specific non-financial regulation with its own section in an SEC Annual Report? Well, it’s because MSHA can and will shut you down. And they do not care if it makes your shareholders mad.

I don’t spend much time looking at mining stocks, but when given the chance, I always look at the Mining safety disclosures. As an example, Arch Resources, a coal miner, has this handy table attached to the bottom of its 10-k:

They list violation counts, fines, and incidents for each asset. As someone who craves as much data as possible on the equities I’m researching, I love to see it. Not only does this data show real tangible financial risk, but it allows investors to look at companies on a more holistic basis. And as a bonus, putting this regulatory record on display keeps management striving to do better. Other non-mining companies with woeful safety or compliance records can hide their issues in a generic risk factor disclosure on the 10-k. Maybe a sentence or two. Not here. I kinda wish more regulations would be like this.

TCEQ Gets a comeuppance?

The rascally scamps at the Texas Commission on Environmental Quality have been doing a very strange thing for years. This week, a Texas Judge correctly tells them that they may have been breaking the law. Whoops!

One of the hallmarks of American environmental law, especially when it comes to permitting facilities under statutes like the Clean Air Act, is that decisions involving major sources of pollution or environmental impact need to have a public comment and review period. Despite it not being in State Law or in Commission guidance, TCEQ apparently hallucinated a limitation on who can comment on air permit applications, requiring commenters to live within a mile of the facility. They just, like, made up this one mile rule. And started approving permits while denying the consideration of comments using said made-up rule. A Travis County Judge ruled the practice by TCEQ illegal and immediately canceled an Air Permit that was the subject of a lawsuit.

The best part of this story is TCEQ’s media strategy (willful, easily disproved insanity) here:

While a TCEQ spokesperson denied the existence of the one-mile rule when asked about the practice, Inside Climate News compiled a list of 15 cases that centered on the one-mile standard using data assembled by the nonprofit law firms Texas RioGrande Legal Aid and Earthjustice

Anyways, it's a great writeup by the Texas Tribune. Highly recommend reading.

Reg Updates

I’ve spent a few months working on a way to scan and automate new regulatory and legal happenings that can affect publicly traded equities. Still very much in the early phases here, but let me know what you like and what you don’t like about this feature, so feel free to subscribe with this Handy link:

ESG HOUND YEAR END DEAL: 50% off subscriptions

Tickers/Companies mentioned this week

Oil and Gas Operations (Louisiana): ETR 0.00%↑ , DOW 0.00%↑ , CLMT 0.00%↑ , MRO 0.00%↑ , PSX 0.00%↑

Foreign Entites on DOE-backed projects: TSLA 0.00%↑ $TM, F 0.00%↑ , GM 0.00%↑ , CATL, Samsung, LG

FCC shoots ASTS in the Head (via SpaceX): ASTS 0.00%↑

Combustion Sources (refining, oil and gas, chemicals) - EPA Is starting to Crack Down on Startup and Shutdown Emissions, maybe?

Industry Impacted (Primary) : Chemicals, Oil & Gas,

Affected companies: ETR, DOW, CLMT, MRO, PSX

Background: The Clean Air Act is a federal law, but typically administered by individual states through “delegated authority.” The States are allowed to issue permits and enforce laws under the Federal rules though several mechanisms. The primary mechanism is the “State Implementation Plan” (SIP) of the Clean Air Act. Individual states take federal law and add their own state laws and procedures for administering the Clean Air Act under the SIP. EPA reviews these SIPs to make sure they are up to snuff for EPA guidance and federal law.

Louisiana’s SIP was up for review and the EPA has “disapproved” it for a few reasons. The primary cause being that it didn’t like how the State managed startup and shutdown events for sources of emission that generate NOx (a byproduct of combustion and a precursor to regional smog/ozone).

EPA and States have struggled with how to deal with startup and shutdown events and emissions for DECADES. It’s an ongoing battle. The CAA is well set up to manage ongoing steady-state operations (when a plant is humming along). However, control requirements, be it from a flare, catalytic converter, or scrubber are hard to manage during the time when a plant is starting up or shutting down. Think of the huge flaring events you might see during an upset condition. Maintaining NOx, PM or smoke (particulate emissions) is tricky from a technical standpoint. States have traditionally carved out SSM (startup shutdown malfunction) events into separate buckets for this purpose where facilities are allowed to emit more pollution during one of these events. However, as industry is wont to do, there’s been huge abuse of this carveout and states like Louisiana (Oil friendly and conservative/anti-regulation) are more likely to allow the status quo. EPA doesn’t like this “loophole” as Louisiana has implemented it. SIP battles are always fun but the take-home here is that EPAy usually (but not always) wins a SIP battle when they pick it.

This SIP argument, should EPA win, will start trickling down into renewal and new permitting in Louisiana in 2-3 years. The fight is specific to NOx (combustion) emissions at large sources in the Baton Rouge → New Orleans corridor but could include additional capital costs at refineries, compressor stations, gas plants and

Dollars and Cents:

Estimating the costs of an EPA win here is tricky but I would tack an additional $10 million to large refinery project modification in the future and an additional $1-3 million for new and reconstruction gas plants and power plants (especially natural gas).

Expect larger and more expensive flare and control equipment, higher penalties for shutdowns, and additional permitting headaches in Louisiana.

This is more of a macro look at how EPA (under the Biden admin, so caveats apply!) may tackle the SSM issue.

Potential Impact: 🔶Neutral/Insignificant in the short run but possibly NEGATIVE for refiners, and midstream in the medium term

Foreign Entity of Concern Update - DOE makes its interpretation for subsidy applicability (China mostly)

Industry Impacted (Primary) : Autos

Industry Impacted (Secondary) : Batteries, Chips, Solar Panels

Affected companies: $TSLA, $TM, $F, $GM, $CATL

Background: The Inflation Reduction Act brought with it a boon of current and future subsidies for green energy and electric vehicles. Lawmakers, notably Hawks like Joe Manchin, pushed for strict and concrete limitations on foreign entities the US doesn’t have open trade agreements with and even stricter limitations on “Foreign Entities of Concern,” which includes businesses with connections to North Korea, Russia, Iran, but most importantly, China.

There’s a reason Automakers and those in the supply chain have been fretting for months:

David Schwietert, chief policy officer for the Alliance for Automotive Innovation, underscored what he said is a vital need for lawmakers to offer greater clarity regarding the Inflation Reduction Act’s sourcing guidance before they are implemented in six months.

“Right now, the industry, we’re working closely with Treasury, but we need certainty because from a supply chain standpoint, January is not that far away,” he said. “You don’t just wake up tomorrow at any one of these companies and say, ‘you know what, go find another cathode or anode producer because I don’t know what the rules are.’”

DOE’s interpretation of the standard is here. I won’t cover it in depth but in regards to Chinese companies, this portion of the definition of an entity is key

(iv) An entity organized under the laws of the United States that is owned by, controlled by, or subject to the direction (as interpreted in Section IV) of an entity that qualifies as a foreign entity in paragraphs (i)–(iii).

What this means is that a foreign company will be excluded from subsidy and tax offset benefits if the following applies:

(i) 25% or more of the entity's board seats, voting rights, or equity interest are cumulatively held by that other entity, whether directly or indirectly via one or more intermediate entities; or

(ii) With respect to the critical minerals, battery components, or battery materials of a given battery, the entity has entered into a licensing arrangement or other contract with another entity (a contractor) that entitles that other entity to exercise effective control over the extraction, processing, recycling, manufacturing, or assembly (collectively, “production”) of the critical minerals, battery components, or battery materials that would be attributed to the entity.

Chinese-held companies would have to have less than 25% of the equity and voting rights if they want to create a subsidiary AND there is wide latitude for the government to deny tax benefits if there are agreements in place to handle input goods (such as metals rare earth minerals) that run exclusively through Chinese entities. The key phrase here is “exercise effective control.”

Dollars and Cents:

With a time-adjusted value of potentially over $1 trillion in the next 10 years (yes, it’s a CATO link, but the analysis tracks), this is huge.

Outlook: I am not a lawyer. The thing to look out for here is the public comments as they roll in. That will give a good indication of who is mad and who is thrilled.

Potential Impact: MASSIVELY 🔴🔴🔴 NEGATIVE FOR THE LOSERS and MASSIVELY 🟢🟢🟢 POSITIVE FOR THE WINNERS

Satellite Spectrum Licence to SpaceX - FCC Might have Shot ASTS 0.00%↑ in the head

Industry Impacted (Primary) : Telecom, Space

Affected companies: $ASTS

Background: AST SpaceMobile has $140 million in Net cash. They’ve burned about that much in the past year and have a small constellation of satellites that sometimes works. They want to make direct satellite to mobile internet a reality. SpaceX/Starlink is the 800 pound gorilla in the room in satellite internet.

The FCC just issued a license for SpaceX to launch 840 demo/test satellites in the first half of 2023. These Starlink units would be equipped to provide D2D (direct to cell) service, directly stomping on AST’s target market. The FCC clearance also seems to pave the way for global application. The spectrum approval would come after a successful test campaign

Dollars and Cents:

ASTS currently has a market capitalization of $1.1 billion and no similar FCC approval. They do not have the financial resources to stay afloat, much less keep up with the SpaceX juggernaut.

Outlook: I’ll leave this one to my friend Tim Farrar

Potential Impact: ASTS, previously only 90% certain to go bankrupt, is all but certainly worth $0 in the coming year or two. RIP