That “Hamas Shortseller” Study is Impossibly Bad

Let’s talk about a law professor. His name is Joshua Mitts.

Professor Mitts has an insanely impressive CV. A JD from Yale and PhDs in Finance and Econ from Columbia. He teaches at Columbia Law School. Sadly, Josh is a walking advertisement for the maxim that “a degree is just a piece of paper” because this guy has embarrassed himself more than any famous academic in recent memory (non-Jordan Peterson category) due to repeated, rudimentary errors he makes in a field he has supposedly mastered.

Mitts got a little fame for himself a few years back in 2018, when the recently graduated Doctorate correctly deduced some suspicious activity associated with put options on Farmland Partners (FPI) stock. His report landed on the desk of FPI management, who then went on to succesfully sue the short-seller, Quinton Matthews.

Mitts, a gainfully employed academic, took full advantage of the resulting positive PR about his work. Companies routinely threaten to fight back against dastardly short-sellers, but most established firms who do this sort of activist investing are generally much more careful than Matthews was. The FPI fallout suddenly inspired many other companies to want to sue short-sellers. Mitts gladly took their money to consult in their (often ill-inspired) battles:

After Farmland, several other companies trying to repel short sellers hired him to consult, including Banc of California Inc (BANC.N), Burford Capital Ltd (BURF.L) and Neovasc Inc (NVCN.TO), according to court and regulatory filings.

Since 2018, the now 36-year-old professor has become something of a short-selling conspiracy truther, releasing absolutely garbage pre-print studies on his Columbia Law webpage and then selling his services to flailing companies looking for empty wins against people who dare say mean things about their poorly run businesses.

Mitts has also offered his services to the SEC, gladly becoming a face of the “shorts hate American businesses” campaign. The SEC initiated a probe into short-sellers in 2021, which resulted in several high-profile funds being raided by the FBI. Mitts likely wasn’t the sole inspiration for this investigation, but he certainly has made a name for himself in highlighting the narrative that many shorts are acting unethically. Mitts is also an expert witness for the SEC, with the agency apparently willing to accept his “expertise” in the field at face value.

Mitts’ behavior certainly is troubling on the surface. Releasing flawed studies under cover of his sparking academic credentials and offering paid consulting services to companies who want to punish shorts while acting as an expert to the agency responsible for enforcing security trading violations represents numerous conflicts of interest.

With Mitts’ very cool and ethical business promoted under an Ivy League Banner seemingly humming along, the good professor (and co-author Robert J. Jackson from NYU) dropped his latest divination this week, and folks, it’s not great:

Yikes! Mitts has claimed that short sellers are good for the market, but his actions have undermined this contention. In reality, he’s been loudly selling “shorts are the devil” to the 401k-loving public, and they cannot get enough of that stuff. This week's pre-publication study was immediately disseminated in the press.

People with advance knowledge of the Oct. 7 terror attacks on Israel by Hamas may have financially profited from the deadly strikes through significant short-selling of shares in Israeli companies, a study says.

“Days before the attack, traders appeared to anticipate the events to come,” says the research paper by U.S. financial law specialists.

“Our findings offer strong evidence that informed traders profited by anticipating the events of October 7,” according to the unpublished study that notes the specific reasons behind such unusual trading is not known, but suggests twisted insider trading could be a means of terrorist financing or terror profiteering.

I read the paper Monday after these news articles came out. “Terrorist Group Hamas are also shorts-sellers” has got to be one of the most click-worthy combinations of words ever written down in the history of Business Press slop, and hoo boy did it work.

Sadly for Mitts, the head of the Israeli stock exchange quickly disputed the magnitude of his claim:

They wrote that for investors in Leumi (LUMI.TA), Israel's largest bank, 4.43 million shares sold short over the period Sept. 14 to Oct. 5 yielded profits of 3.2 billion shekels ($859 million).

But the Tel Aviv Stock Exchange (TASE) said the authors miscalculated, because share prices are listed in agorot, which are similar to cents and pence, rather than shekels - putting the potential short sale profit at just 32 million shekels.

A 100x error on currency calculation is, uh, kind of a big deal! Remember that this was published on a Columbia University Website. And sold to the press. And Mitts is an expert witness for the SEC. Not great. Imagine the outcry if a notable short seller made an error on a key financial metric by two orders of magnitude.

But here’s the thing. Sure, a $8.59 million profit is a bit less sexy than a $859 million dollar profit. And let’s be honest here: no one in their right mind would put it past a bunch of murderous terrorists to make a little side-money betting on stocks from its violent rampage on October 7th.

But Mitts’ paper is bad for so many reasons. I’ll show you what I mean. The core premise of the "research” presented is that Mitts and Jackson could tell the shorts knew about the attacks because of a spike in FINRA short volume data on October 2nd:

Nearly 100% of the FINRA reported volume in an Israeli Stock ETF (EIS) was sold short just five days before they attacked Israel. This sounds bad, right? Well… FINRA short volume data isn’t comprehensive. In fact, it’s probably a less-than-worthless statistic since most of the required volumes reported are in Dark Pools, where large credentialed funds trade assets outside of public exchanges. I feel like it’s reasonable to assume Hamas was not running their trades through an institutional trade desk.

Intra-day total short volumes are notoriously hard to separate from regular buys and sells. This is why specialized firms charge an arm and a leg for an estimate of short volume using proprietary data tools. Mitts, in his own paper, kinda admits this!

Under Regulation SHO, each exchange must publish daily short volume data for short sales on that exchange, but every exchange now charges a substantial fee to obtain these data. By contrast, FINRA makes these data available for free for trades reported to its trade reporting facilities…

“Sure, there is more comprehensive data available, but we can’t afford to pay THAT,” is sure one way to justify your data acquisition methods.

Putting all of that aside, let’s take a look at the FINRA data ourselves and see what this is all about.

The first thing I did was grab FINRA data for the same “spike” data of October 2nd; this is the same data used by Mitts. I filtered the data set for International ETFs and reported short interest above 90%. Here’s is the result:

As we can see from the above chart, by 10/2/23, Hamas had plans in place to attack one of the following countries:

Canada

The United Kingdom

Israel

Brazil

Denmark

Norway

Egypt

They ultimately settled on terrorizing their Arch-nemesis, Israel. I guess Hamas didn’t have enough boats to go after the infidels in Norway.

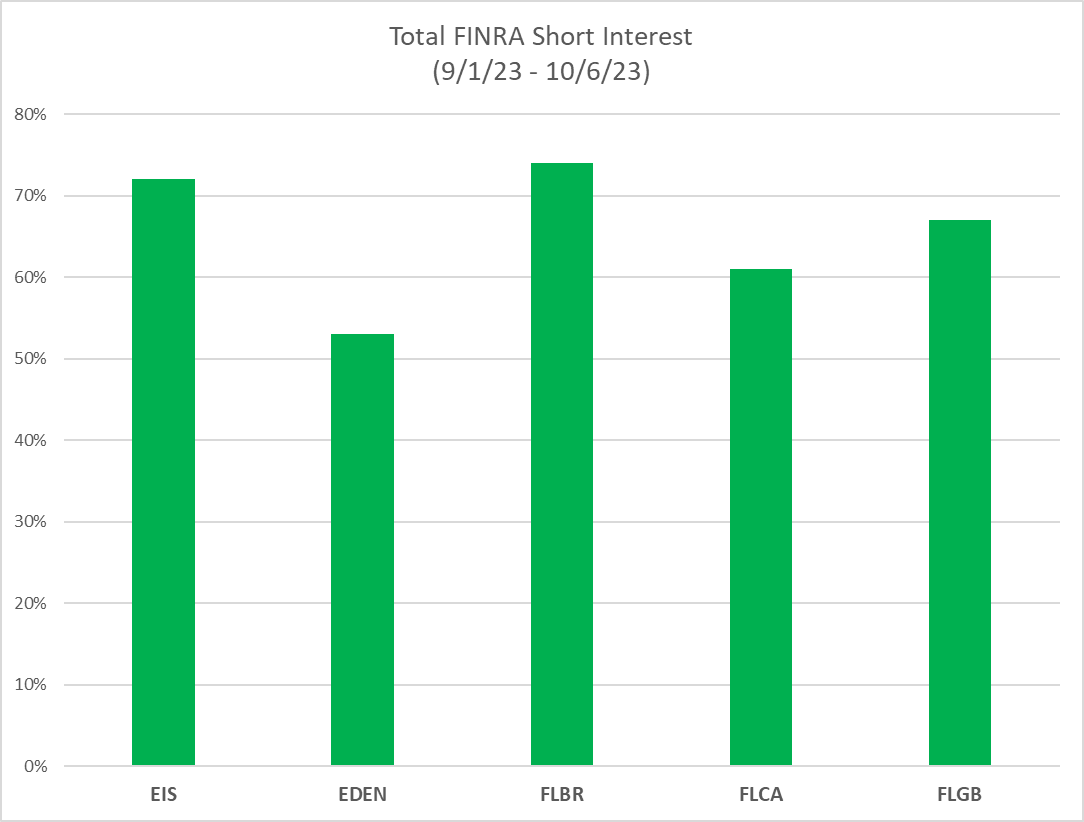

In all seriousness, this is roughly the level of rigor seen in Mitts’ and Jackson’s analysis, as they failed to look at market-wide dynamics, factor trading, rebalancing, and quant positioning. Relative to the market, the spike in FINRA shorts against the Israeli ETF (which has under $200 million of total assets, by the way) was far from unusual as there were several country ETFs (FLCA, FLGB, FLBR, EDEN) with a nearly identical short percentage and dollar value placed against them.

This is pretty cut-and-dry evidence that the authors started with the preposition that Hamas is making money by being a naughty short seller and then contorted themselves to prove it. Bad stuff here.

But let’s take it a step further:

Using the five ETFs with nearly identical short volume (~$12 million) on 10/2 and comparing the Short Interest for Israel ETF (EIS) vs an average, volume-weighted composite of the other four ETFs, Mitts and Jackson’s “spike” chart doesn’t look so impressive:

There is admittedly a lot of noise in the data, but we can see that short interest in these products more or less moves in tandem, directionally, during the same time period referenced in this study.

Taking a step back, the TOTAL short interest over the same time period is probably the best tell:

Proving a negative is notoriously difficult, but I think it’s safe to say that the “evidence” that Hamas was shorting Israeli stocks based on FINRA data is objectively lousy research.

Former Harvard president Larry Summers, another bumbling academic who keeps landing absurdly cushy gigs, got himself into trouble back in 2005 for stating that Women don’t succeed as often as men in STEM fields because of their inferior brains. Not so, Dr. Summers! Josh Mitts is evidence that the absence of any brain activity whatsoever is certainly no barrier to getting multiple fancy degrees and cover to pontificate on subjects one does not understand.

If you enjoyed this piece, please mash the heart button and share it with your favorite Law Professor on Social Media.

This piece sucked up all my free time over the past few days. The weekly news wrap and PREMIUM REG UPDATE should be zipped to your email box tomorrow or Friday.

Here’s a 50% off coupon for ESGH premium good until the end of the year if you want to support my work:

👉CLICK HERE FOR AN AMAZING DEAL

And as always, hugs and kisses, all. Eric