Enovix - You've Been Scammed? Maybe (part 2)

The company's deal with YBS doesn't make any sense

So you’re hyping a battery company? In 2023?

It’s pre-revenue? And trading at a $3 billion valuation?

But hold on! The company has plans for a new factory?

And the deal is based on a non-binding Letter of Intent?

With a Malaysian Nano Cap????

Welcome to the Thunderdome

Last week, I released the first part of my research on Enovix, the California Based, 15-year-old, battery startup. I knew things were contentious around this stock and company, but I think I underestimated the scale and scope of it all. It was a fairly straightforward piece about a company whose statements to permitting authorities didn’t line up with what they told investors.

Interestingly, most of the feedback was positive and constructive. But some people in The Thunderdome (Twitter) were not super thrilled with my post! These folks attacked me personally without engaging in the facts laid out. I haven’t seen anyone address the facts in my piece when criticizing it, which I take as a good sign. When you don’t have the facts on your side, you go right to the kick in the groin.

But this publication isn’t about social media drama. Neither was my first post about Enovix. And guess what? This post isn’t about that, either.

We’re doing the same thing we did last time. Full access to paid subs on day one and unlocked for everyone to read tomorrow. (edit: post unlocked!) If you like the work I do and think it provides value, I’d love to have you on as a paid subscriber. If not, that’s ok too. Check back in later.

Here’s a link for 20% off a subscription → CLICK ME!

Malaysian Dreams

Now that we have that fun stuff out of the way, let’s continue from where we left off in part 1. With Fab-1 output projections drastically slashed, Enovix management pivoted to Malaysia, where Fab-2 would do what Fab-1 couldn’t: produce batteries for sale on the market.

Western audiences tend to treat “Asian” economies as three different buckets: China, Japan, and Other. China is a powerhouse of manufacturing and research. Japan: a mature, high-tech, but low-growth economy. The “Other” bucket includes South Korea, India, and smaller southeast Asian economies such as the Philippines, Vietnam, Malaysia, Laos, Cambodia, Indonesia, and Bangladesh.

Westerners tend to lump these southeastern countries into an indistinguishable pile. To this audience, these countries are defined by cheap labor and industrial processes that were once the stereotypical “Chinese” enterprises. Clothing, plastic stuff, widgets, cheap electronics.

Of course, these countries are, in reality, unique and vibrant, each with their own quirks, resources, strengths, and risks. The real world is messy. To contextualize this story, we need to understand some things about Malaysia. I’m not going to claim some sort of specific expertise here, so please correct me if I’ve mischaracterized or generalized anything. Here are the highlights, based on conversations I’ve had with several analysts and businesspeople I trust:

Malaysia used to be really corrupt

Malaysia is less corrupt than it was

The Malaysian government really wants to bring in investment dollars from the West

Malaysian legal records aren’t very easy to acquire or analyze

The track record for Malaysian PR Announcements isn’t great!

American and Western understanding of Asian companies is far too often steeped in racist and/or 20th-century tropes. We’re going to try our hardest to avoid anything that makes us look foolish here. Malaysia is growing quickly. In 2009, the country’s GDP was $202 billion. GDP for 2021 was $373 billion and should exceed $400 billion in the next few years. A doubling in 15 years is pretty good, but for proper context, it should be noted that Chinese GDP will have increased nearly four-fold in the same time period. American GDP is up 65% since 2009.

Malaysia is a legal black box to outsiders, so it’s not shocking that fraudsters have shown an affinity for using the country for their good old-fashioned American Stock Promotes. But the country is also bringing in real investment dollars. Samsung, for example, broke ground on a $1.3 billion battery plant in Malaysia in 2022. This is real progress and a big win for the country’s desire to replace labor-intensive, cheap goods manufacturing with high-tech industry that spurs economic growth and demand for STEM degree-holders.

Enovix is not Samsung, however. When Samsung points at a map and says “We are going to build a factory here,” we all can agree that this is a tradeable, factual, and uncontroversial statement.

When Enovix wants to build a factory, they sign a non-binding Letter of Intent with a Malaysian nanocap. There are more red flags than words in the preceding sentence, so perhaps it’s best to look at the past history of American-listed companies issuing a non-binding LOI with a Malaysian partner. Here is a list of all SEC 8-k filings since 2008 that mention such a business arrangement, along with outcomes:

October 2008 - Ecolocap (ECOS) signs a non-binding letter of intent with Heibe Xinneng Power Corp for the development of a biomass powerplant in Hebei, China. ECOS’s suppliers they were negotiating with were Malaysian-based.

5 Year Equity Return: -98.3%

Current Status: ECOS delisted as of April 2021

July 2011 - Vystar (VYST.OB) signs a non-binding LOI with Malaysian based EcoGlove Asia Pacific Sdn Bhd to merge the companies. Vystar made a product called “Natural Rubber Latex” and EcoGlove made, well… gloves. This LOI was terminated in September 2011. Vystar is no longer a going concern.

5 Year Equity Return: -100%

Current Status: Trading on the pink sheets

January 2014 - Well Power, Inc (WPWR), a Nevada Registered corporation with corporate offices in Malaysia, signed a non-binding LOI with Canadian inventor Cristian Neagoe to license his definitely-not-vaporware Green Fuel™ Microrefinery. The LOI was not consummated and the company was effectively bankrupt within 6 months

5 Year Equity Return: -100%

Current Status: WPWR delisted in August 2015

August 2017 - Contact Minerals Corp (CNTM), a Nevada-based mining company, enters an agreement to sell their shares of the defunct company to Malaysian investors Shiong Han Wee and Kwueh Lin Wong. The reverse merger was intended to fast-track US Stock market listing and the company changed its name to WECONNECT Tech International (WECT) upon consummation in November 2017. In June of 2018, the company bought 99.662% of the shares of another Malaysian company, MIG Mobile Tech Bhd and:

The Company was never able to profitably operate the MTT business. The Company incurred a net operating loss of $1,103,166 for the year ended July 31, 2020, and an

accumulated deficit of $7,638,503 as of July 31, 2020.

The SEC took serious issues with the company’s June 2020 10-K filing, a bunch of insiders sold everything and company shareholders were subsequently diluted by 90%. It is now called Motos America and they sell cars in Florida or something. I don’t really care.

5 Year Equity Return: -97%

Current Status: The company is now selling shares via Reg D

January 2021 - Agape ATP Corporation (OTCPK:AATP) signs non-binding LOI to purchase 51% of shares of two Malaysian companies: DSY Wellness & Longevity Center Sdn. Bhd. and DSY Medical Education Sdn. Bhd. In a shocking twist, this merger and subsequent joint venture were consummated in November 2021.

2.5 Year Equity Return: -10%

Current Status: AATP trades on the OTC exchange with a $450M valuation

March 2023 - Sino Green Land Corp (SGLA), a Malaysian-based fruit vendor, signed a Non-binding LOI to buy sister company Sino Green Land Corp (of Malaysian territory Labuan). This is a related party transaction and involved issuing lots of stock, so the company shares dropped by a third in a single day.

Three Month Equity Return: -33%

Current Status: SGLA trades on the OTC exchange with an $800,000 valuation

While I cannot claim this list is definitively exhaustive, I was not able to find a single 8-k (or similar) LOI agreement involving a Malaysian company that did not end in tears. If you, dear reader, can find one single example of such an arrangement that had positive economic outcomes, I will gift you a one-year membership to this publication.

YBS International - Your Battery Source?

Enovix’s non-binding Letter of Intent with YBS came directly on the heels of their announcement that Fab-1 was kind of a dud. Fab-2 would be the real game-changer, folks!

Malaysia’s government obviously wants to bring in outside capital (understandable). They would also like to avoid having another whoopsie like 1MDB (likewise understandable). The government has cleaned up its act significantly since. However, a starting point of “the largest kleptocracy case to date” investigated by the US Department of Justice means that even with drastic improvement, things can still be, uh, sketchy.

In an attempt to (1) bring in outside capital, (2) keep at least some of that capital within its borders, and (3) continue growing domestic GDP, the Malaysian government has some tools at its disposal. The 1MDB remains a bloated corpse of bad debt that will take many more years to fully unwind. 1MDB was, at the time, the single cornerstone for the country’s goal to spur local development and entice outside investors. The government wants to keep doing that stuff, so they’ve instead put resources into smaller, nominally independent organizations, primarily those owned by the Ministry of Finance. They’ve also allowed private companies to do due diligence. It’s basically a bunch of separate government-controlled bags of money instead of a single slush fund.

The country has also reorganized some regulatory bodies, fired a ton of officials and committed to better transparency in the future. The Malaysian government would love nothing more than to claim that the underlying systemic problems are fixed since 2016, but the self-dealing, fraud, and embezzlement embedded into the government's very fabric from top to bottom are pretty hard to correct.

This World Bank report from 2021 is a great short read. While overall sunny in its outlook, the report notes four big issues that remain unresolved:

Federal Changes at the top were drastic but “need to be cascaded to other levels of government, namely states and local authorities.”

An overwhelming majority of Malaysian media remains controlled by the government. If the people writing checks (responsible for nearly 50% of industrial and tourism CapEx in the country in 2021 nationwide) are also the same people who control the news, it is hard for accountability to be enforced via reporting.

The Proposed Public Service Act, which keeps getting announced but not passed, would provide “clarity and accountability in the approval process, appointments, rewards, and performance management, amongst others, and strong governance structures.” Government actions and appointments are still frustratingly unclear and obtaining public records is a nightmare.

(Aside: it cost me $40 per hour to access court and business records for this publication, and the data is incredibly sparse)

“The reform of the GLCs and state-owned enterprises is on-going and it is unclear if the next stage of reforms would include those at the subnational levels.” The World Bank kind of gives away the narrative here, basically stating that the large 1MDB slush fund that was broken down into smaller (potential slush) funds is a mechanical solution and may create the same problems in the future.

Ok! My takeaway, and I confirmed this with sources in Malaysia and elsewhere in Asia, in both finance and law, is that the problem isn’t solved on a granular or local level. The runaway fraud and embezzlement amoeba that was 1MDB was quarantined mechanically, but many of the conditions that led to its creation are still present. Given the recentness and scale of the 1MDB collapse, local officials have at least more awareness and hesitancy to straight-up shopping out bribes, appointments, and contracts in the open. Humiliation FTW!

One of the Ministry of Finance-owned organizations that took up some of the check-writing duties following 1MDB is the Malaysian Industrial Development Finance Corporation (MIDF). They issued an RM60 Million ($13 million) credit facility to one YBS International Bhd in 2021. The interest rates associated with this facility were in the 4-6% range at the time of their July 2022 annual report. The 10 Year interest rate on Malaysian Government Bonds averaged around 4% for the year. A <200 bp cost above the government rate is quite good, especially for a small company in a developing market.

YBS International sports a market capitalization of around $35 million and has a net debt of negative $6 Million. Earnings were $700k on 17% gross and 3.5% net margins in the most recent fiscal year. Revenue growth has been 19% over the past two years. It trades at 50x trailing earnings. The margins aren’t surprising considering they make cardboard, CNC-milled doohickies, and mold-injected plastic stuff.

YBS trades at like 50x earnings. A little steep if you ask me, but whatever, it’s up 40% in the past year; stocks do that sometimes. Oddly enough, the company’s stock is flat since the announcement they’d be the home of Enovix’s world-class, industry-disrupting battery of the future. But before we go forward, let’s go back in time.

This interview with company management from March of 2022 and looking at how they’ve performed since is a good place to start.

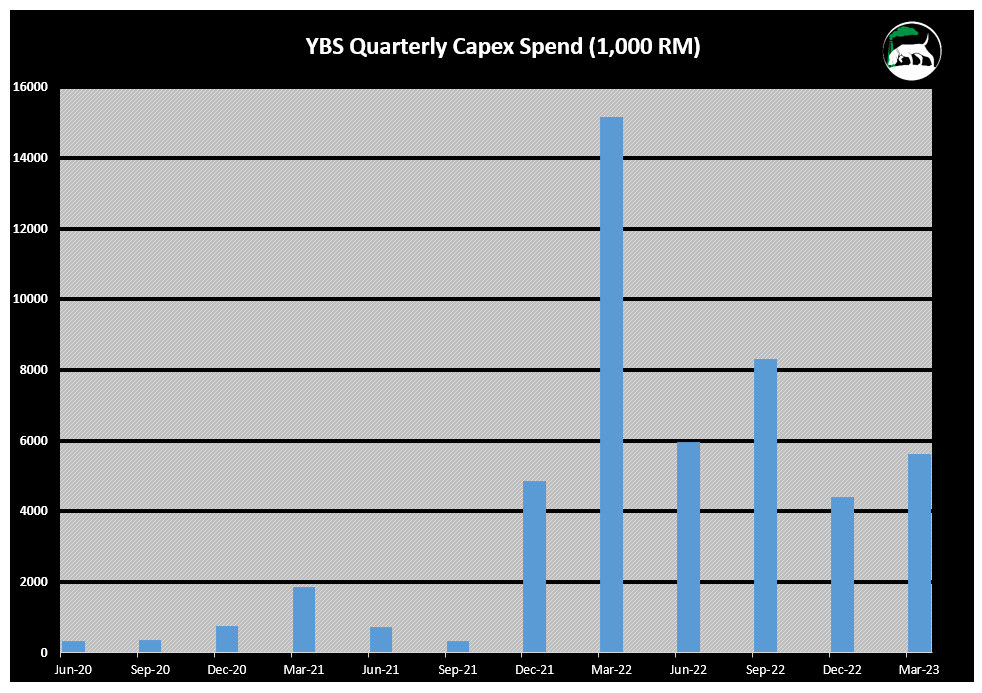

The company committed to spending RM45 million ($10 million) on just their Penang Science Park facility (future home of Enovix!) over the next two years.

Total company CapEx since that interview (during the March 22 Quarter) has been RM35 Million. I estimate Capex associated with the Penang facility is about 70% of total Capex, meaning they’re something like halfway towards their RM45 million goal with a few quarters remaining. All good here.

On the revenue projections front, things look a tad more dicey:

All in all, the group will be able to achieve RM200 million in revenue by the financial year ending March 31, 2024 (FY2024), he says.

Already, YBS’s contracts in hand could generate revenue of RM160 million to RM180 million “in a year”, says Yong, but the actual booking of revenue will depend on the purchase orders signed by its customers on a monthly basis.

The latest reported quarter (March 2023) had revenues of RM24 Million, which annualizes to RM96 Million, or less than 50% of the projected RM200 Million sales figure from last year. Here’s where you numbers nerds might start sweating alongside me.

RM35 Million in CapEx to increase annualized revenues from RM80 Million (first quarter post Covid Shutdown reopening) to 100 Million (most recent quarter), for a company that sports a woeful 3.5% operating margin is not great. Even backing out the interest costs of capital, that 20 million in sales generates only RM 700k, which would pay down the invested capital at zero percent interest in about 50 years. Bad!

Maybe they’re “ramping” on an “s-curve” or something. I don’t know

What I do know is that while the out-of-data imagery on Google Earth shows this for their factory:

…the remainder of the factory was completed in Early November 2022 and showed up on the Sentinal2 satellite data set:

Speaking purely hypothetically, let’s say you spent a bunch of money on a factory using government-backed loans in a state where there has been some scrutiny on how the government gives out checks to private companies. Perhaps your once cheery prospects of selling RM160 to RM180 million in goods next year with only the “contracts you have in hand” don’t look as good as they once did.

A hot California company (they’re neighbors with Tesla!) comes knocking. You’ve got factory space, they’ve got lots of very excited investors, and a market capitalization 100 times bigger than yours. All you’ve gotta do is, let’s see here… take out a loan of up to $70 Million from your local government-run banks, bringing your net debt from negative $6 million to as high as positive $64 million, or almost two times your own market capitalization.

Do you sign a non-binding Letter of Intent with the California battery company? Heck yeah you do! No obligation, tons of optionality, plus it can’t hurt to ask the government for a low cost loan that dwarfs all your existing assets combined.

I’m not being facetious at all, by the way. This is a no-brainer. Plus YBS management gave way more details than Enovix did to their American investors.

When exactly was the contract signed?

Enovix: March 2023

YBS: On March 16th, we finalized the terms of the agreement. Our company signed the letter on March 23rd, and Enovix signed it on March 29th.

Are there any other conditions?

Enovix: …

YBS: The letter is expected to be formalized in three months time from the agreement date, which was March 16th

You might notice that the current date here on Earth is July 13th, 2023, which is coming up on *four* months since the LOI date. And a bunch of stuff has happened since then.

March 29th - Enovix announces the LOI with YBS and ENVX stock goes up 21%

April 17th - Enovix announces the sale of $150 million in convertible senior notes. The stock is up 18% since the announcement of the LOI and up 80% year to date.

May 25th - 🚨BOTH of YBS’s Corporate Secretaries resign on the same day 🚨

June 9th - News is released that the bank YBS uses for its existing $13 Million government-backed loan (Malaysian Industrial Development Finance Bhd) is being acquired by a non-government entity, the Malaysian Building Society Bhd, an investment holding and banking firm. 👀

June 15th - ENVX drops a press release that they hit their quarterly production goal of 18,000 watch batteries with two weeks to spare! Never mind that Fab-1 capacity was supposed to be 45 Million units (or 5,136 cells per hour) as recently as last year. That’s 3.5 hours of production from previous guidance.

June 16th - Three months have passed since the LOI was signed. There’s a provision for mutual extension, but no update from either party on where it stands.

June 27th - Enovix blasts out another press release. They were chosen to submit battery cells as a subsupplier to a government contractor for US Army equipment in pre-production builds of some equipment. What is the size of the contract? Where will the Cells Be Made? Is the offer contingent on anything? Is it an ongoing contract or a one-time deal? The answer to these questions is a resounding “We don’t know because they didn’t tell us!” Fantastic.

This timeline, to me, does not demonstrate the natural and bullish progression on the LOI and getting the company ENVX closer to making batteries. It makes me feel like something doesn’t quite add up.

Given that, let’s tie it all together.

Takeaways

If I were silly enough to short any stock, and especially silly enough to short this stock with a particularly credulous and passionate shareholder base, I would ask myself “What am I missing?” I would also ask “How do I hedge myself in case the trade goes against me?”

Likewise, if I were long a pre-revenue, speculative stock that was up nearly 3x in six months, I would ask myself “Am I sure I believe the story?” and “When is a good time to take some money off?”

I have some records and follow-ups coming my way shortly, including some from Malaysia that may (or very much may NOT) be helpful, so there will certainly be more from me. But I looked at this story today almost entirely from the Standpoint of YBS and its shareholders.

And there are some huge red flags. In many Asian countries, Malaysia included, the Corporate secretary is a unique and very important person. The government requires these officers to act as the eyes and ears of regulatory compliance. They are required to be born natural-born citizens of the country and are licensed through a central authority. They receive better compensation than other people with similar roles in private companies, and they have by far the lowest turnover rates of any corporate official in Malaysia. Paying these employees is the explicit trade-off for having a publicly listed company in the country. It’s a protection against too much foreign influence and is intended to prevent excess capital flight.

Multiple Asian equity followers have told me that a single licensed secretary departure is a cause for concern. Two at once? “Unheard of” and “A huge red flag.”

And then there is the banking question. Does a change in bank ownership matter when the fundamentals of any sort of imaginable terms for such a loan (up to $70 Million on $35 million in Market cap!!!!) require explicit government backing?

You’ve got to consider the 1MDB scandal too. The government might want any and all foreign capital they can get, but also… backing a loan involving a pre-revenue de-SPAC using a tiny company that makes little commodity parts and cardboard boxes might be a step too far, even if everything is on the up-and-up.

Let’s not forget the delays, the increasingly bizarre and non-specific press releases from ENVX themselves and, and, and…

Because you can yell at me about how good the battery technology is, how amazing the sales funnel is, point at a pyramid-shaped chart that goes over the TAM for these perfect and beautiful batteries. But. A huge part of the bull case involves ENVX getting to market. And right now, that path goes through Malaysia and YBS. If that deal fails, even through no fault of Envonix or YBS, that’s a bad outcome for ENVX shareholders.

What if the deal does go through? Which equity does better? ENVX, which has tripled in three months? Or YBS, which would double its annual earnings with every $700k dropped to the bottom by hosting their hyped American partners? I know which I’d choose.

Bonus Content

In researching this piece, I found one of the most hilarious shareholder meeting transcript quotes of all time, courtesy of Location Based Technologies, Inc. Although completely unrelated to the piece, I wanted you to enjoy it:

Next item is without question the most important task on this list, and that is to achieve profitability. Even though we haven’t closed our fourth quarter yet, we know we’re not quite going to make it. Although this is a big disappointment for all of us, we are getting close. In fact, as recently as a couple of months ago I thought we were going to hit this milestone. We have 1 large pending order from an international corporation that would have made us cash flow positive had the LOI closed.

Until next time…

Disclosure: This report is the sole work of me, Eric Roesch. I was not paid or commissioned to write it. However, as an independent contractor, I currently provide research and advisory services to financial firms, funds, startups and companies, public and private alike. As such, assume I am short shares of ENVX and stand to make money in the event this equity decreases in value.

Fun to read. I love it when charlatans are compromised with some good humor.